Disclaimer: All of the information provided in this article is my personal opinion and is meant for entertainment and information purposes only. I am not a professional in the field but just a guy on the internet. Make sure you do your own research and consult with a professional such as a financial planner or a CPA before making investment decisions.

What is a stock?

A stock represents a share in the ownership of a company and gives you a claim on part of the company’s assets and earnings. By owning stock, you own a small part of the company and become a shareholder. Stock is considered an asset because you may receive dividends, which are payments from the company’s earnings. Sometimes, a company reinvests its earnings back into the business, increasing its fundamental value over time. Either way, a stock has inherent value because the company itself has value, which includes assets like buildings, offices, factories, intellectual property, and more.

A company’s growth is driven by profits. Employees seek to earn a living and build careers, investors want to grow their investments, and governments benefit from the tax revenue generated by income and economic activity. This dynamic promotes growth, innovation, and economic turnover. In general, most capitalist governments and institutions around the world support the growth and success of the stock market. Whether or not you think the system is flawed, the likelihood of a total collapse and the world descending into a zombie apocalypse is very low. Therefore, it’s important not to make decisions about your financial future based on fear or misinformation.

That said, the stock market does carry risks. Companies have gone bankrupt in the past and will likely do so in the future. The key to managing this risk is diversification—spreading your investments across a large number of companies rather than putting all your money into one or a few. This strategy reduces the risk associated with any single company’s performance.

How much do Stocks return?

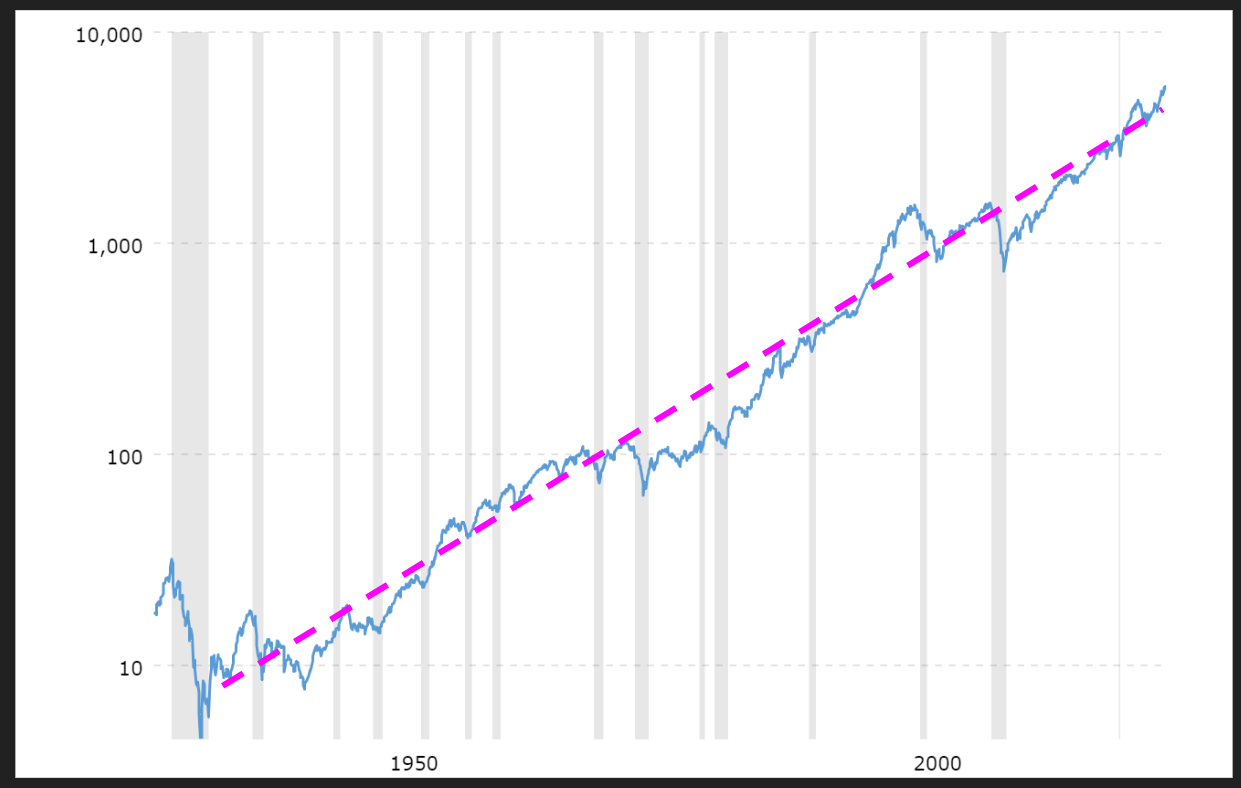

A good way to represent the value of the stock market is through an index. For the U.S. domestic stock market, one of the most popular indices is the Standard and Poor’s 500 (S&P 500). This index tracks the performance of 500 of the largest publicly traded companies in the United States. Looking at the historical data for the S&P 500 over the last 90 years, we see a general upward trend, despite periods of fluctuation. On a log scale, the index shows growth over time, with both rises and dips. While we can’t predict the future with certainty, the long-term trend suggests that the stock market will likely continue to grow in the future.

Now, let’s look at the same plot without the log scale. In this version, the early decades may appear almost flat, even though growth is still happening. This is why a log scale is useful for understanding long-term trends—it helps reveal consistent growth over time, even when the early stages seem less dramatic.

If we calculate the average annualized compound interest rate for the last 90 years in the stock market, it comes to about 10% per year. Over the same period, the average inflation rate has been about 3%. After adjusting for inflation, the inflation-adjusted annualized return is approximately 7%. This is the return I generally expect from the stock market over the long run, and I often use this figure in my projections and calculations.

It’s important to note that this 7% return is expected in the long run. Over short time frames, the market is unpredictable, with many unexpected events causing fluctuations. These could be market corrections, bear markets, or recessions. Let’s take a look at the frequency of these market movements:

- A market correction is defined as a decline of 10% or more, and these happen fairly often. Based on historical data since 1928, a correction occurs roughly every 1.7 years.

- A bear market is characterized by a decline of 20% or more. Bear markets are less frequent than corrections but tend to last longer, sometimes several months or even years. Historically, a bear market has occurred approximately every 4.5 years.

- A recession is a significant decline in economic activity across the economy, typically defined by two consecutive quarters of negative GDP growth. Since 1928, there have been 14 recessions, which averages to about one recession every 7 years. Recessions tend to have long-lasting effects, sometimes persisting for years, with significant economic impacts and rising unemployment.

The big picture here is that market downturns are a natural part of the stock market. However, over the long run, the market tends to rise. By understanding and preparing for these downturns, you can navigate the volatility and capitalize on the market’s growth potential to build your investments.

How much do bonds return?

A bond represents a loan made by an investor to a borrower, typically a government or corporation. In exchange for the loan, the issuer promises to repay the principal amount on a specified maturity date and to make periodic interest payments to the bondholder until that date. In other words, as an investor, you receive a return on your investment in the form of interest payments from the borrower.

Bonds are different from stocks and can play an important role in your investment portfolio, particularly for the purpose of diversification. While bonds are generally considered safer investments than stocks, they also tend to provide lower returns. Bonds usually (but not always) have an inverse correlation to the stock market, meaning that when stock prices decline, bond prices or interest rates often rise. U.S. government bonds, in particular, are considered among the safest investments in the world, which is why their returns are relatively low compared to riskier assets like stocks or corporate bonds.

Basics of investing in stock market:

One of the fundamental principles of investing is that risk and reward are proportional. We expect higher returns from riskier investments, and as the risk decreases, so do the potential returns. Stocks, also known as equity, typically offer higher returns but are more volatile, meaning they fluctuate up and down frequently, carrying higher risk. Bonds, on the other hand, especially government bonds, are less risky and provide smaller returns on investment.

When building an investment portfolio, it’s essential to structure it according to your risk tolerance. A good way to manage risk is by having both stocks and bonds in your portfolio, adjusting the proportions based on your risk tolerance, goals, and the stage of your life. As your circumstances change, you can periodically rebalance your portfolio to maintain your desired asset allocation.

As mentioned earlier, the ups and downs of the market are a natural part of the investment journey. Remember that stock market investing is for the long term, typically meaning 10 years or more. If you are saving for something in the short term, like a house down payment in the next 3-5 years, the stock market is not the right place for that money.

It’s also important to understand the psychology of investing. Avoid falling into the trap of thinking, “it’s different this time,” and resist the urge to panic or make rushed decisions. Likewise, don’t get seduced by promises of unrealistic market returns. As Warren Buffet famously said, “Be fearful when others are greedy and greedy when others are fearful.” Developing the ability to overcome fear and FOMO (fear of missing out) is key to becoming a successful investor.

Additionally, ensure that your brokerage account is covered by SIPC insurance. This insurance protects your assets in the brokerage account—up to $500,000—in the event that the brokerage firm goes bankrupt. However, SIPC insurance does not protect against losses from bad investments; it only safeguards your assets in case of the brokerage’s insolvency.

Mutual fund

A mutual fund is an investment vehicle that pools money from many investors to purchase a diversified portfolio of securities, such as stocks, bonds, or other assets. Mutual funds are typically offered by brokerage companies and managed by a fund manager and their team. The fund manager makes decisions about where to invest the pooled money, with the goal of generating capital gains or income for the investors.

However, managing a mutual fund comes with costs. The fund manager and their team need to be paid, and the brokerage company that offers the fund also needs to make a profit. Additionally, there are costs associated with advertising the fund, and some mutual funds have sales charges or upfront fees.

One common fee is the 12(b)-1 fee, which covers the costs of marketing, distributing, and servicing the fund. Some funds also have a redemption fee or exit fee, meaning you’ll be charged when you sell or redeem shares of the fund within a certain period. Every time assets in the fund are bought or sold, trading fees are incurred as well. Depending on your type of account, you may also have to pay short-term or long-term capital gains taxes when assets are sold.

A good mutual fund should ideally have no upfront or exit costs, and the 12(b)-1 fees related to advertising, distribution, and marketing should be as low as possible, ideally $0. In today’s market, paying these extra fees often doesn’t add value for the investor and mainly benefits the brokerage company or the fund manager.

Expense ratio

The expense ratio is a measure of the total annual cost of owning a mutual fund, exchange-traded fund (ETF), or other investment fund, expressed as a percentage of the fund’s average net assets. It includes management fees, administrative fees, operating costs, and other expenses associated with running the fund. For example, an expense ratio of 1% means that 1% of the fund’s asset value is deducted each year to cover fees, regardless of whether the fund makes a profit. The expense ratio directly impacts investors’ net returns because these costs are taken out of the fund’s assets.

For instance, if the investments in the fund grew by 8% in a given year and the expense ratio was 1%, your effective return would be 8% – 1% = 7%. This reduction directly affects your bottom line as an investor.

In my opinion, an expense ratio of 1% or higher is excessively high. Personally, I wouldn’t invest in any fund with an expense ratio of 0.5% or higher, as these fees can significantly reduce your overall returns over time.

Index funds

An index fund is a type of mutual fund designed to replicate the performance of a specific financial market index, such as the S&P 500. Unlike actively managed funds, where fund managers select individual securities to buy and sell, index funds aim to match the performance of the market index they track by holding the same securities in the same proportions as the index. This eliminates the need for active management by a fund manager, which keeps fees low. As a result, index funds often have expense ratios of less than 0.1%.

A great example of an index fund is the Vanguard 500 Index Fund (VFIAX), which follows the S&P 500 index. The expense ratio for this fund is currently 0.04%. Another example is the Vanguard Total Stock Market Index Fund (VTSAX), which tracks the performance of the entire U.S. domestic stock market, also with an expense ratio of 0.04%.

It’s important to note that the S&P 500—which represents the top 500 companies in the U.S. domestic stock market—accounts for 80% of the market capitalization, or 80% of the money in the market. While there are thousands of other index fund options available, major brokerage companies like Vanguard, Fidelity, and Charles Schwab offer some of the most popular and low-cost options. For instance:

- Schwab S&P 500 Index Fund (SWPPX) has an expense ratio of 0.02%.

- Fidelity 500 Index Fund (FXAIX) has an expense ratio of just 0.015%.

Since index funds simply track a market index, there isn’t much active decision-making by fund managers, nor is there significant turnover of stocks within the fund. The management is mostly passive, as the fund merely follows the market index it is designed to replicate.

Historically, it has been observed that, over the long term, most actively managed mutual funds fail to outperform the stock market as represented by market indices. These actively managed funds also come with higher expense ratios and unnecessary overhead costs, which can amount to hundreds of thousands of dollars in lost returns over several decades.

By contrast, an index fund—especially a broad market-based one—is passive, low-cost, diversified, and therefore one of the best vehicles for long-term growth.

Exchange Traded Funds or ETFs

To invest in a mutual fund or index fund, you typically need to create a brokerage account with the company offering that fund. While some brokerages allow you to invest in funds from other companies, this often comes with hefty fees, which is not ideal. However, if you already have a brokerage account with a company that doesn’t offer the specific index fund you want, you can still invest in the ETF version of that fund, if that’s offered in the market.

An ETF (Exchange-Traded Fund) is essentially the stock version of a mutual fund. You can buy ETFs through any brokerage account, just like you would buy a stock. For example, if you have an eTrade account and want to invest in the Vanguard 500 Index Fund (VFIAX), you can’t directly invest in VFIAX, but you can buy the ETF version in the open market by purchasing VTI (Vanguard Total Stock Market ETF), which trades like a stock.

There are no additional fees associated with buying an ETF compared to investing directly in the index fund—the expense ratio is built into the ETF itself, so the cost to the investor is the same. The only difference is that you have to buy ETFs in whole shares. For example, at the time of writing, VTI is trading at $282.35. So if you have $300 to invest, you can only use $282.35 to buy 1 share of VTI, with the remaining money uninvested. While this isn’t a big issue once your portfolio grows larger, it’s something to be mindful of to avoid leaving too much of your money uninvested.

If you have a brokerage account with the company that offers the index fund directly, you can invest in the mutual fund version and put your entire amount into the fund without having to worry about share prices. However, many index funds have a minimum investment requirement. For example, VFIAX has a minimum of $3,000 to get started. By contrast, ETFs typically have no minimum investment requirement, making them easier to get started with for new investors.

Summary

The stock market is a powerful tool for building wealth and is critical for your Financial Independence journey. While there are short-term risks, the market has historically been a solid place for long-term investments. Don’t let fear or lack of knowledge dictate your financial decisions—educate yourself, understand the risks, and invest wisely. Broad market index funds should play a key role in your investment portfolio due to their low cost, diversification, and passive management.